AYUSHMAN BHARAT

IN NEWS

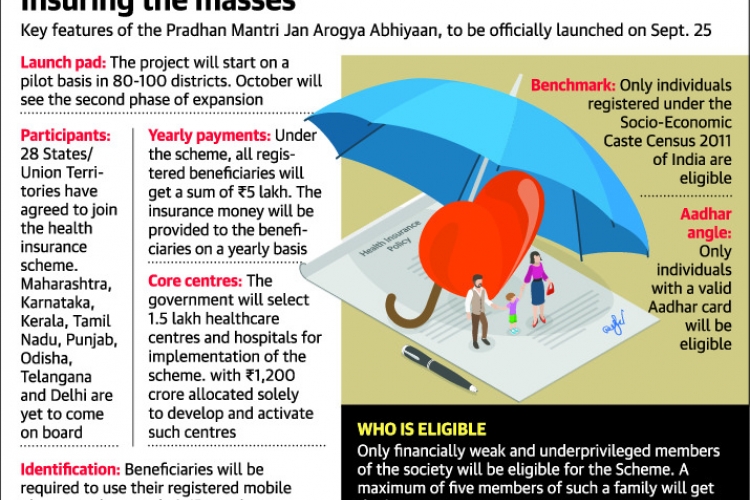

In Independence Day speech, Prime Minister Narendra Modi said that his government will launch the ambitious Ayushman Bharat healthcare scheme on September 25, 2018. Modi's Ayushman Bharat scheme, touted as the world's largest healthcare scheme, aims to provide a coverage of Rs. five lakh per family annually. The Ayushman program has been designed to address the current deficiencies in the public sector healthcare industry, infrastructure, including lack of funds and resources.

ABOUT THE SCHEME

Ayushman Bharat - National Health Protection Mission will subsume the on-going centrally sponsored schemes - Rashtriya Swasthya Bima Yojana (RSBY) and the Senior Citizen Health Insurance Scheme (SCHIS).

The fundamental objective is to strengthen secondary, primary and tertiary healthcare system in India and it also focuses on offering financial protection during an emergency situation for all needy families.

BENEFICIARIES

Beneficiaries included are the poor, deprived rural families and identified occupational category of urban workers' families, 8.03 crore in rural and 2.33 crore in urban areas, as per the latest Socio Economic Caste Census (SECC) data.

MAJOR INITIATIVES

- Ayushman Bharat - National Health Protection Mission will have a defined benefit cover of Rs. 5 lakh per family per year.

- Benefits of the scheme are portable across the country and a beneficiary covered under the scheme will be allowed to take cashless benefits from any public/private empanelled hospitals across the country.

- Ayushman Bharat - National Health Protection Mission will be an entitlement based scheme with entitlement decided on the basis of deprivation criteria in the SECC database.

- To control costs, the payments for treatment will be done on package rate (to be defined by the Government in advance) basis.

- One of the core principles of Ayushman Bharat - National Health Protection Mission is to promote co-operative federalism and flexibility to states.

- For giving policy directions and fostering coordination between Centre and States, it is proposed to set up Ayushman Bharat National Health Protection Mission Council (AB-NHPMC) at apex level Chaired by Union Health and Family Welfare Minister.

- States would need to have State Health Agency (SHA) to implement the scheme.

- To ensure that the funds reach SHA on time, the transfer of funds from Central Government through Ayushman Bharat - National Health Protection Mission to State Health Agencies may be done through an escrow account directly.

- In partnership with NITI Aayog, a robust, modular, scalable and interoperable IT platform will be made operational which will entail a paperless, cashless transaction.

Implementation Strategy

At the national level to manage, an Ayushman Bharat National Health Protection Mission Agency (AB-NHPMA) would be put in place. States/ UTs would be advised to implement the scheme by a dedicated entity called State Health Agency (SHA). They can either use an existing Trust/ Society/ Not for Profit Company/ State Nodal Agency (SNA) or set up a new entity to implement the scheme.

States/ UTs can decide to implement the scheme through an insurance company or directly through the Trust/ Society or use an integrated model.

EXPENDITURE INVOLVED

The expenditure incurred in premium payment will be shared between Central and State Governments in specified ratio as per Ministry of Finance guidelines in vogue. The total expenditure will depend on actual market determined premium paid in States/ UTs where Ayushman Bharat - National Health Protection Mission will be implemented through insurance companies. In States/ UTs where the scheme will be implemented in Trust/ Society mode, the central share of funds will be provided based on actual expenditure or premium ceiling (whichever is lower) in the pre-determined ratio.

IMPACT OF THE SCHEME

Ayushman Bharat - National Health Protection Mission will have major impact on reduction of Out of Pocket (OOP) expenditure on ground of:

1.Increased benefit cover to nearly 40% of the population, (the poorest & the vulnerable)

2.Covering almost all secondary and many tertiary hospitalizations. (except a negative list)

3.Coverage of 5 lakh for each family, (no restriction of family size)

This will lead to increased access to quality health and medication. In addition, the unmet needs of the population which remained hidden due to lack of financial resources will be catered to. This will lead to timely treatments, improvements in health outcomes, patient satisfaction, improvement in productivity and efficiency, job creation thus leading to improvement in quality of life.

ANALYSIS OF THE SCHEME

1.If the government is going to route the payments through the insurance companies, these companies will be making nearly 30 per cent of the money.For instance, if the government is paying Rs 100, then Rs 30 will go to these insurance companies.Only Rs 70 will be available for expenditure that will be incurred by the hospitals.

Nobody will work to make losses and quality may be compromised which needs review on this aspect.

2.The scheme is good for the public and the country. The ultimate thing are the hospitals (that will be empanelled) that are likely to offer these services to the public.If they are not comfortable doing this the scheme, (Ayushman Bharat) is going to be paralysed.

3.Without proper scientific data it makes no sense to arrive at the cost of a medical service.And the package (cost) that the government has arrived at is not scientific.

4.The other part is that this scheme is meant to cover the lower socio-economic group of people, which is about 45 per cent of the Indian population.All the medium hospitals in India concentrate on this group of people.So, if the government is going to undercut the cost of procedures, then it will be very difficult for these medium-sized hospitals to manage their operations and survive.

The big corporate hospitals, for instance, could even manage by cross-subsidising patients who pay under the NHPS, but the smaller and medium-sized hospitals will be wiped out under the cost burden.

WAY FORWARD

The government must ensure that the service providers (hospitals) are made to feel comfortable by mandating a comfortable package rate.The scheme will be very successful only if empanelled hospitals are comfortable delivering the goods under the NHPS.

The government should take the 'trust' model -- to route payments to the hospitals through a government trust -- instead of the insurance companies.

UPSC - 2027 - Prelims cum Mains - New Batch Starts on 24-06-2026

UPSC - 2027 - Prelims cum Mains - New Batch Starts on 24-06-2026